When you finance a car, you might not realize that the amount you owe could be more than what your car is actually worth. This gap can leave you in a tough spot if your vehicle is stolen or totaled in an accident.

That’s where gap insurance comes in—it covers the difference between your car’s value and the remaining loan balance. If you want to avoid surprising bills and protect yourself from unexpected costs, understanding gap insurance for financed cars is essential. Keep reading to find out how gap insurance works, why it matters to you, and how to get the best coverage without breaking the bank.

What Gap Insurance Covers

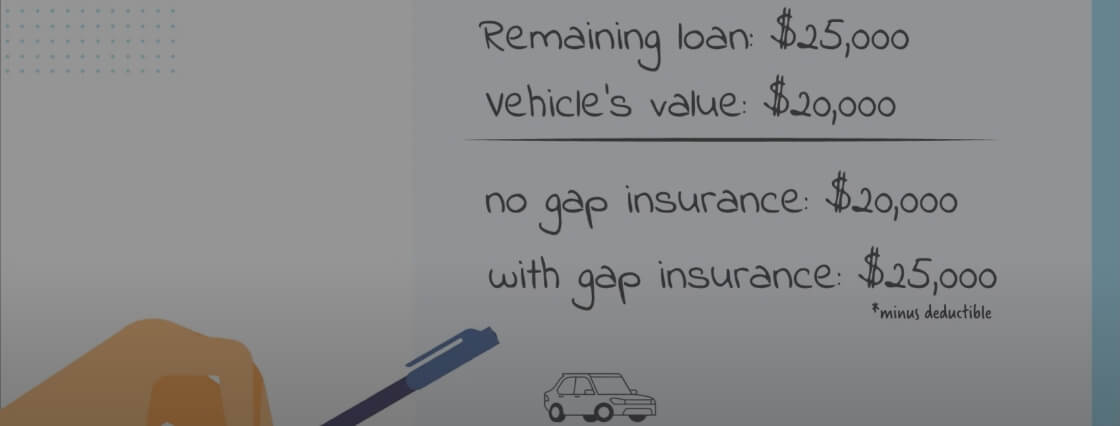

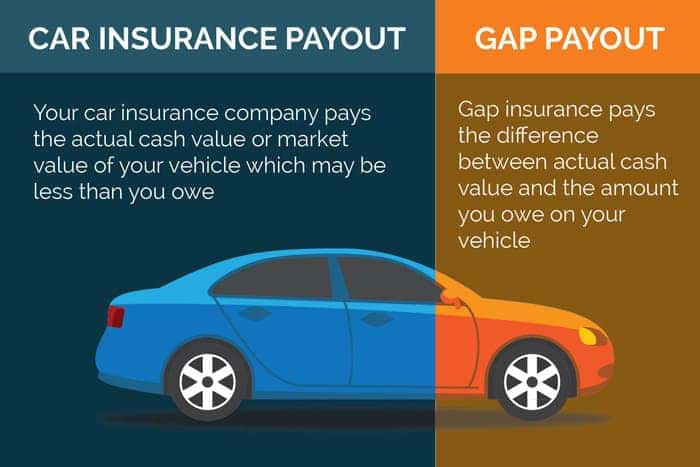

Gap insurance covers the difference between your car’s value and the amount you owe. This is important in total loss scenarios, like theft or accidents. If the car is declared a total loss, standard insurance pays only the current market value. Often, this value is less than the remaining loan or lease balance.

The loan vs. value gap happens because cars lose value quickly after purchase. Depreciation means your car’s worth drops faster than your loan balance. Gap insurance fills this financial gap, protecting you from owing more than the car’s value.

Protection against depreciation is key. Without gap insurance, you might pay out of pocket to clear your loan. This coverage provides peace of mind and helps avoid unexpected expenses after a total loss.

Who Should Consider Gap Insurance

Gap insurance is smart for those who finance their cars. It covers the difference if the car is totaled or stolen. Financed car buyers often owe more than the car’s value early on. Gap insurance helps cover that gap.

Leased vehicle holders should also consider gap coverage. Leased cars can have high fees if totaled. Gap insurance protects against those costs.

Drivers with high loan balances face bigger risks. If the loan amount is close to or higher than the car’s worth, gap insurance is useful. It prevents large out-of-pocket expenses after a loss.

How Gap Insurance Works

The claim process for gap insurance starts after a total loss. First, your standard auto insurance pays the car’s current market value. This value is often less than the amount owed on the loan. Gap insurance then covers the difference between the insurance payout and the loan balance.

Your insurer works directly with the lender. The payment from gap insurance goes to the lender to clear the remaining loan. This ensures you do not owe money for a car you no longer have.

| Step | Details |

|---|---|

| 1. Total Loss Reported | Notify your insurer about the accident or theft. |

| 2. Standard Insurance Payment | Insurer pays the car’s market value. |

| 3. Gap Insurance Payment | Gap insurance pays the remaining loan balance. |

| 4. Lender Receives Payment | Lender gets paid to close the loan. |

Ways To Purchase Gap Insurance

Car dealerships offer gap insurance as part of financing deals. This option is easy but may cost more. Dealers often add extra fees to the price.

Adding gap insurance to your existing auto policy can save money. Many insurance companies let you include it with your collision or comprehensive coverage. This method is usually cheaper and convenient.

| Option | Details | Cost |

|---|---|---|

| Car Dealerships | Included in car financing, quick to get | Often highest price |

| Adding to Auto Policy | Attach to current insurance plan | Usually lower cost |

| Credit Union/Bank | Offers gap insurance as a separate product | Competitive pricing |

Credit unions and banks may sell gap insurance too. They provide separate policies with competitive rates. Check with your bank or credit union for details.

Cost Factors Of Gap Insurance

Loan payoff options can help cover the amount left on your car loan. Some lenders offer programs that reduce your balance faster. This option may save money but can be limited by the lender’s terms.

Extended warranties cover repairs beyond the factory warranty. They do not cover the loan balance but protect against costly repairs. This can keep your car running without extra expenses.

Vehicle replacement programs offer a new or similar car if yours is totaled. These programs often come from manufacturers or dealers. They can be costly but provide peace of mind about car loss.

| Option | What It Covers | Pros | Cons |

|---|---|---|---|

| Loan Payoff Options | Remaining loan balance | May reduce debt faster | Limited by lender terms |

| Extended Warranties | Car repairs | Low repair costs | Does not cover loan balance |

| Vehicle Replacement Programs | New or similar car | Peace of mind | Can be expensive |

Frequently Asked Questions

Should I Get Gap Insurance On A Financed Car?

Gap insurance covers the difference if your financed car is totaled or stolen and you owe more than its value. It protects you from paying out-of-pocket. Consider it if your loan exceeds your car’s worth, especially early in the loan term when depreciation is steep.

How Much Is Gap Insurance For A Financed Vehicle?

Gap insurance for a financed vehicle typically costs between $20 and $50 annually. Prices vary by insurer and coverage options.

What Is The Downside Of Gap Insurance?

The downside of gap insurance includes extra cost and limited coverage duration. It may not cover all fees or loan types. Some dealers charge high markups, increasing your overall expense.

What Does Gap Do When Financing A Vehicle?

Gap covers the difference between your car’s current value and the remaining loan balance if the vehicle is totaled or stolen.

Conclusion

Gap insurance protects you from owing more than your car’s value. It covers the gap between your loan balance and the car’s worth. This coverage can save you money if your car is stolen or totaled. Consider your loan terms and how fast your vehicle loses value.

Choose gap insurance that fits your budget and needs. Review your policy regularly to decide when to cancel. Protect your finances with gap insurance on financed cars. It offers peace of mind during uncertain situations.

Read More

- Pay Per Mile Car Insurance: Save Big with Smart Driving Choices

- Temporary Car Insurance Online: Quick, Affordable Coverage Today

- Zero down Car Finance Deals: Unlock Affordable Driving Today!

- Vehicle Loan Payoff Calculator: Maximize Savings & Pay Off Fast

- Car Loan Prequalification Online: Quick Steps to Secure Approval

- Teen Driver Insurance Cost: How to Save Big and Get Coverage

- Auto Refinance Rates Comparison: Unlock the Best Savings Today

- Mobile Mechanic Service near Me: Reliable, Fast, and Affordable Options

- Transmission Repair Financing: Affordable Options to Save Your Ride

- Engine Repair Cost Estimate: Save Big with Expert Tips Today